Estimation of Price Surfaces¶

![]()

This notebook outlines how to specify different variants the model, then proceeds to fit them.

Imports¶

#exports

import pandas as pd

import numpy as np

import os

import pickle

from tqdm import tqdm

from moepy import lowess, eda

import seaborn as sns

import matplotlib.pyplot as plt

User Inputs¶

models_dir = '../data/models'

load_existing_model = True

Loading & Cleaning Data¶

We'll start by loading in ...

%%time

df_EI = eda.load_EI_df('../data/raw/electric_insights.csv')

df_EI.head()

Wall time: 1.69 s

| local_datetime | day_ahead_price | SP | imbalance_price | valueSum | temperature | TCO2_per_h | gCO2_per_kWh | nuclear | biomass | coal | ... | demand | pumped_storage | wind_onshore | wind_offshore | belgian | dutch | french | ireland | northern_ireland | irish |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2009-01-01 00:00:00+00:00 | 58.05 | 1 | 74.74 | 74.74 | -0.6 | 21278 | 555 | 6.973 | 0 | 17.65 | ... | 38.329 | -0.404 | nan | nan | 0 | 0 | 1.977 | 0 | 0 | -0.161 |

| 2009-01-01 00:30:00+00:00 | 56.33 | 2 | 74.89 | 74.89 | -0.6 | 21442 | 558 | 6.968 | 0 | 17.77 | ... | 38.461 | -0.527 | nan | nan | 0 | 0 | 1.977 | 0 | 0 | -0.16 |

| 2009-01-01 01:00:00+00:00 | 52.98 | 3 | 76.41 | 76.41 | -0.6 | 21614 | 569 | 6.97 | 0 | 18.07 | ... | 37.986 | -1.018 | nan | nan | 0 | 0 | 1.977 | 0 | 0 | -0.16 |

| 2009-01-01 01:30:00+00:00 | 50.39 | 4 | 37.73 | 37.73 | -0.6 | 21320 | 578 | 6.969 | 0 | 18.022 | ... | 36.864 | -1.269 | nan | nan | 0 | 0 | 1.746 | 0 | 0 | -0.16 |

| 2009-01-01 02:00:00+00:00 | 48.7 | 5 | 59 | 59 | -0.6 | 21160 | 585 | 6.96 | 0 | 17.998 | ... | 36.18 | -1.566 | nan | nan | 0 | 0 | 1.73 | 0 | 0 | -0.16 |

... and cleaning the GB data

df_EI_model = df_EI[['day_ahead_price', 'demand', 'solar', 'wind']].dropna()

s_demand = df_EI_model['demand']

s_price = df_EI_model['day_ahead_price']

s_dispatchable = df_EI_model['demand'] - df_EI_model[['solar', 'wind']].sum(axis=1)

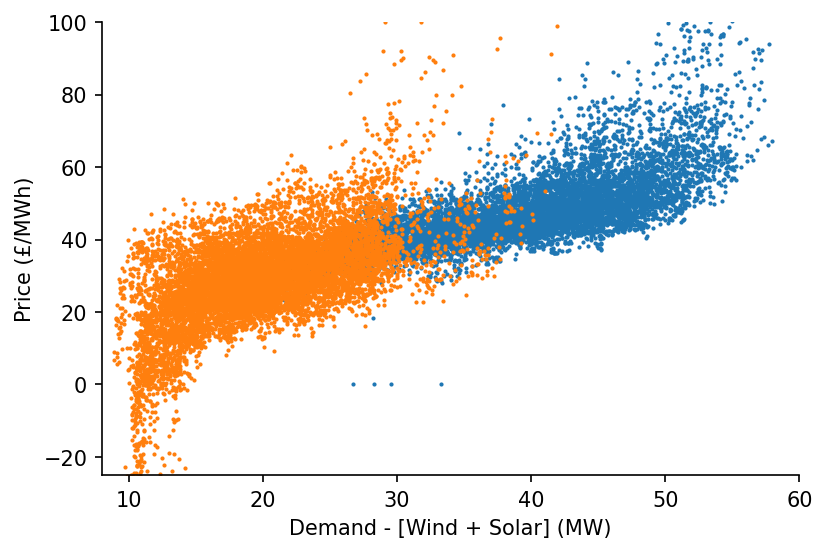

# Plotting

fig, ax = plt.subplots(dpi=150)

ax.scatter(s_dispatchable['2010-09':'2011-03'], s_price['2010-09':'2011-03'], s=1)

ax.scatter(s_dispatchable['2020-03':'2020-09'], s_price['2020-03':'2020-09'], s=1)

eda.hide_spines(ax)

ax.set_xlim(8, 60)

ax.set_ylim(-25, 100)

ax.set_xlabel('Demand - [Wind + Solar] (MW)')

ax.set_ylabel('Price (£/MWh)')

Text(0, 0.5, 'Price (£/MWh)')

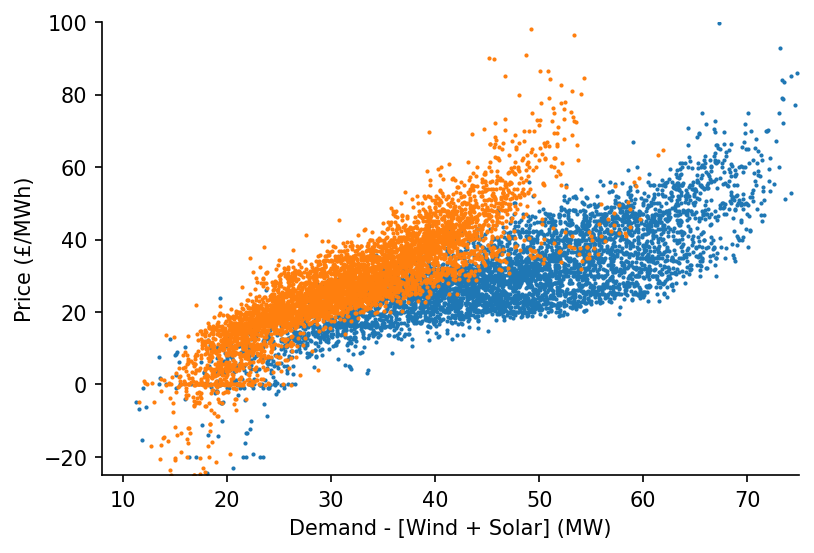

As well as the DE data

df_DE = eda.load_DE_df('../data/raw/energy_charts.csv', '../data/raw/ENTSOE_DE_price.csv')

df_DE_model = df_DE[['price', 'demand', 'Solar', 'Wind']].dropna()

s_DE_demand = df_DE_model['demand']

s_DE_price = df_DE_model['price']

s_DE_dispatchable = df_DE_model['demand'] - df_DE_model[['Solar', 'Wind']].sum(axis=1)

# Plotting

fig, ax = plt.subplots(dpi=150)

ax.scatter(s_DE_dispatchable['2015-09':'2016-03'], s_DE_price['2015-09':'2016-03'], s=1)

ax.scatter(s_DE_dispatchable['2020-03':'2020-09'], s_DE_price['2020-03':'2020-09'], s=1)

eda.hide_spines(ax)

ax.set_xlim(8, 75)

ax.set_ylim(-25, 100)

ax.set_xlabel('Demand - [Wind + Solar] (MW)')

ax.set_ylabel('Price (£/MWh)')

Text(0, 0.5, 'Price (£/MWh)')

Results Wrapper¶

We'll start defining each of the price models that we'll fit, using the PicklableFunction class to ensure that all of our models can be saved for later use.

#exports

import copy

import types

import marshal

class PicklableFunction:

"""Provides a wrapper to ensure functions can be pickled"""

def __init__(self, fun):

self._fun = fun

def __call__(self, *args, **kwargs):

return self._fun(*args, **kwargs)

def __getstate__(self):

try:

return pickle.dumps(self._fun)

except Exception:

return marshal.dumps((self._fun.__code__, self._fun.__name__))

def __setstate__(self, state):

try:

self._fun = pickle.loads(state)

except Exception:

code, name = marshal.loads(state)

self._fun = types.FunctionType(code, {}, name)

return

def get_fit_kwarg_sets(qs=np.linspace(0.1, 0.9, 9)):

"""Helper to generate kwargs for the `fit` method of `Lowess`"""

fit_kwarg_sets = [

# quantile lowess

{

'name': f'p{int(q*100)}',

'lowess_kwargs': {'reg_func': PicklableFunction(lowess.calc_quant_reg_betas)},

'q': q,

}

for q in qs

# standard lowess

] + [{'name': 'average'}]

return fit_kwarg_sets

model_definitions = {

'DAM_price_GB': {

'dt_idx': s_dispatchable.index,

'x': s_dispatchable.values,

'y': s_price.values,

'reg_dates_start': '2009-01-01',

'reg_dates_end': '2021-01-01',

'reg_dates_freq': '13W', # 13

'frac': 0.3,

'num_fits': 31, # 31

'dates_smoothing_value': 26, # 26

'dates_smoothing_units': 'W',

'fit_kwarg_sets': get_fit_kwarg_sets(qs=[0.16, 0.5, 0.84])

},

'DAM_price_demand_GB': {

'dt_idx': s_demand.index,

'x': s_demand.values,

'y': s_price.values,

'reg_dates_start': '2009-01-01',

'reg_dates_end': '2021-01-01',

'reg_dates_freq': '13W', # 13

'frac': 0.3,

'num_fits': 31, # 31

'dates_smoothing_value': 26, # 26

'dates_smoothing_units': 'W',

'fit_kwarg_sets': get_fit_kwarg_sets(qs=[0.5])

},

'DAM_price_DE': {

'dt_idx': s_DE_dispatchable.index,

'x': s_DE_dispatchable.values,

'y': s_DE_price.values,

'reg_dates_start': '2015-01-04',

'reg_dates_end': '2021-01-01',

'reg_dates_freq': '13W', # 13

'frac': 0.3,

'num_fits': 31, # 31

'dates_smoothing_value': 26, # 26

'dates_smoothing_units': 'W',

'fit_kwarg_sets': get_fit_kwarg_sets(qs=[0.16, 0.5, 0.84])

},

'DAM_price_demand_DE': {

'dt_idx': s_DE_dispatchable.index,

'x': s_DE_demand.values,

'y': s_DE_price.values,

'reg_dates_start': '2015-01-04',

'reg_dates_end': '2021-01-01',

'reg_dates_freq': '13W', # 13

'frac': 0.3,

'num_fits': 31, # 31

'dates_smoothing_value': 26, # 26

'dates_smoothing_units': 'W',

'fit_kwarg_sets': get_fit_kwarg_sets(qs=[0.5])

}

}

We'll now take these model definitions to fit and save them

#exports

def fit_models(model_definitions, models_dir):

"""Fits LOWESS variants using the specified model definitions"""

for model_parent_name, model_spec in model_definitions.items():

for fit_kwarg_set in tqdm(model_spec['fit_kwarg_sets'], desc=model_parent_name):

run_name = fit_kwarg_set.pop('name')

model_name = f'{model_parent_name}_{run_name}'

if f'{model_name}.pkl' not in os.listdir(models_dir):

smooth_dates = lowess.SmoothDates()

reg_dates = pd.date_range(

model_spec['reg_dates_start'],

model_spec['reg_dates_end'],

freq=model_spec['reg_dates_freq']

)

smooth_dates.fit(

model_spec['x'],

model_spec['y'],

dt_idx=model_spec['dt_idx'],

reg_dates=reg_dates,

frac=model_spec['frac'],

threshold_value=model_spec['dates_smoothing_value'],

threshold_units=model_spec['dates_smoothing_units'],

num_fits=model_spec['num_fits'],

**fit_kwarg_set

)

model_fp = f'{models_dir}/{model_name}.pkl'

pickle.dump(smooth_dates, open(model_fp, 'wb'))

del smooth_dates

fit_models(model_definitions, models_dir)

100%

4/4

[00:00<00:00, 0.00s/it]

100%

2/2

[00:00<00:00, 0.00s/it]

100%

4/4

[00:00<00:00, 0.00s/it]

100%

2/2

[00:00<00:00, 0.00s/it]

We'll load one of the models in

%%time

if load_existing_model == True:

smooth_dates = pickle.load(open(f'{models_dir}/DAM_price_GB_p50.pkl', 'rb'))

else:

lowess_kwargs = {}

reg_dates = pd.date_range('2009-01-01', '2021-01-01', freq='13W')

smooth_dates = lowess.SmoothDates()

smooth_dates.fit(s_dispatchable.values, s_price.values, dt_idx=s_dispatchable.index,

reg_dates=reg_dates, frac=0.3, num_fits=31, threshold_value=26, lowess_kwargs=lowess_kwargs)

Wall time: 2.7 s

And create a prediction surface using it

%%time

x_pred = np.linspace(8, 60, 521)

dt_pred = pd.date_range('2009-01-01', '2021-01-01', freq='1W')

df_pred = smooth_dates.predict(x_pred=x_pred, dt_pred=dt_pred)

df_pred.head()

Wall time: 346 ms

| Unnamed: 0 | 2009-01-04 | 2009-01-11 | 2009-01-18 | 2009-01-25 | 2009-02-01 | 2009-02-08 | 2009-02-15 | 2009-02-22 | 2009-03-01 | 2009-03-08 | ... | 2020-10-25 | 2020-11-01 | 2020-11-08 | 2020-11-15 | 2020-11-22 | 2020-11-29 | 2020-12-06 | 2020-12-13 | 2020-12-20 | 2020-12-27 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 8 | -7.66001 | -7.78927 | -7.91081 | -8.02572 | -8.13481 | -8.23875 | -8.33813 | -8.43345 | -8.52519 | -8.61382 | ... | 10.2354 | 10.292 | 10.3476 | 10.4021 | 10.4557 | 10.5085 | 10.5611 | 10.6143 | 10.6691 | 10.7271 |

| 8.1 | -7.46772 | -7.59637 | -7.71734 | -7.83171 | -7.94028 | -8.04374 | -8.14266 | -8.23754 | -8.32887 | -8.41709 | ... | 10.4429 | 10.4994 | 10.5548 | 10.6092 | 10.6627 | 10.7154 | 10.7679 | 10.821 | 10.8758 | 10.9336 |

| 8.2 | -7.27561 | -7.40364 | -7.52404 | -7.63785 | -7.74592 | -7.84889 | -7.94734 | -8.04178 | -8.13268 | -8.22049 | ... | 10.6503 | 10.7066 | 10.7619 | 10.8162 | 10.8695 | 10.9222 | 10.9746 | 11.0276 | 11.0823 | 11.1401 |

| 8.3 | -7.08366 | -7.21108 | -7.33089 | -7.44416 | -7.5517 | -7.65418 | -7.75217 | -7.84616 | -7.93663 | -8.02403 | ... | 10.8576 | 10.9138 | 10.9689 | 11.023 | 11.0763 | 11.1288 | 11.1812 | 11.2341 | 11.2888 | 11.3464 |

| 8.4 | -6.89188 | -7.01867 | -7.13789 | -7.25061 | -7.35763 | -7.45962 | -7.55713 | -7.65067 | -7.74071 | -7.82769 | ... | 11.0648 | 11.1208 | 11.1757 | 11.2298 | 11.2829 | 11.3353 | 11.3876 | 11.4405 | 11.4951 | 11.5527 |